Life insurance is a fundamental component of a sophisticated financial strategy, yet for many, the choice between term and whole life insurance remains a point of significant confusion. Selecting the right policy is not merely a matter of picking a monthly premium; it is a long-term decision that impacts your estate planning, tax obligations, and your family’s future security. This article provides an in-depth analysis of these two primary insurance models, exploring their mechanics, benefits, and drawbacks to help you make an informed decision.

Understanding Term Life Insurance: Pure Protection

Term life insurance is often described as the most straightforward form of life insurance. It provides coverage for a specific period, or “term,” typically ranging from 10 to 30 years. If the insured individual passes away during this period, the insurer pays a death benefit to the designated beneficiaries. If the term expires and the insured is still living, the coverage simply ends unless the policy is renewed or converted.

The Mechanics of Term Policies

One of the primary appeals of term life insurance is its simplicity. Because it does not include a savings or investment component, the premiums are significantly lower than those of whole life insurance. This allows individuals to purchase a high amount of coverage for a relatively small monthly fee, making it an ideal choice for young families or those with significant short-to-medium-term financial obligations, such as a mortgage or children’s tuition fees.

Why Choose Term Life?

The primary advantage of term life is affordability. It is designed to replace income during the most vulnerable years of a person’s financial life. For example, a 30-year term policy can cover a parent until their children are grown and the mortgage is paid off. At that point, the need for a large death benefit may diminish, and the policyholder can choose to let the coverage lapse without having lost significant capital.

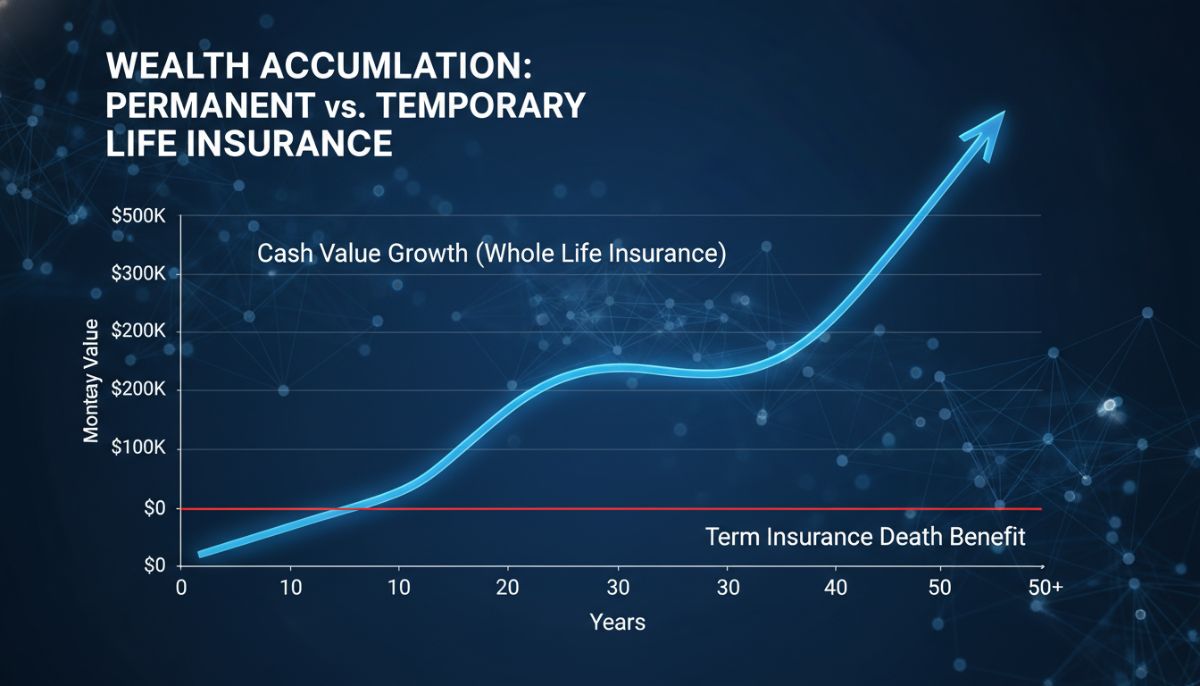

Whole Life Insurance: Permanent Coverage and Asset Accumulation

Unlike term insurance, whole life insurance is a type of permanent life insurance. As long as the premiums are paid, the policy remains in effect for the duration of the insured’s life. This type of policy serves a dual purpose: it provides a death benefit to beneficiaries and includes a “cash value” component that grows over time.

The Cash Value Component

A portion of every premium payment in a whole life policy is funneled into a cash value account. This account grows at a guaranteed rate set by the insurance provider. Over time, the cash value can become a significant asset. Policyholders can borrow against this value, use it to pay premiums, or even surrender the policy for its cash value. Because of this investment element, whole life insurance is often viewed as a financial tool for wealth transfer and estate planning rather than just a safety net.

Tax Advantages and Stability

Whole life insurance offers unique tax benefits. The growth of the cash value is tax-deferred, meaning you do not pay taxes on the gains as they accumulate. Furthermore, the death benefit is generally paid to beneficiaries free of federal income tax. For high-net-worth individuals, whole life insurance can be a strategic way to manage estate taxes and ensure that heirs receive a liquid inheritance.

Critical Comparison: Analyzing the Core Differences

To choose between the two, one must analyze several key factors: cost, duration, and investment potential.

1. Cost (Premiums): Term life premiums are fixed for the duration of the term and are much cheaper. Whole life premiums are also fixed but are significantly higher—sometimes five to ten times more than term insurance for the same death benefit amount—because they cover the cost of permanent insurance and the cash value accumulation.

2. Duration: Term is temporary; whole life is permanent. If you outlive your term policy, your beneficiaries receive nothing. With whole life, as long as the policy is active, a payout is guaranteed upon your death.

3. Flexibility and Loans: Term life offers no liquidity. Whole life allows you to take out policy loans, providing a source of emergency funds or capital for other investments.

Determining the Right Fit for Your Financial Profile

The “better” policy depends entirely on your personal financial goals and current stage of life.

When Term Life is the Better Option

Term life is generally recommended for those who:

- Need maximum coverage at the lowest possible price.

- Want to cover a specific debt or financial responsibility (e.g., a 20-year mortgage).

- Prefer to “buy term and invest the difference,” choosing to manage their own investments in the stock market rather than through an insurance company’s cash value account.

- Have lifelong dependents, such as a child with special needs who will require financial support long after the parents are gone.

- Are in a high tax bracket and seek tax-advantaged ways to grow wealth.

- Want a guaranteed death benefit for estate planning or to cover final expenses (funeral costs, etc.).

- Value the discipline of forced savings that the cash value component provides.

When Whole Life is the Better Option

Whole life may be the superior choice for those who:

Conclusion

The debate between term and whole life insurance is not about which product is objectively superior, but which one aligns with your financial roadmap. Term insurance offers high-leverage protection during your peak earning years, while whole life insurance serves as a permanent asset that integrates insurance with long-term wealth management. Before committing to a policy, it is advisable to consult with a certified financial planner to ensure your choice supports your broader economic objectives and provides the peace of mind you and your family deserve.