Understanding Your Homeowners Insurance Policy: A Comprehensive Guide to Protecting Your Investment

Introduction to Homeowners Insurance

For the majority of individuals, a home is not merely a place of residence; it represents the most significant financial investment of their lifetime. Protecting this asset against unforeseen circumstances is not just a matter of financial prudence but a necessity for long-term stability. A homeowners insurance policy is a complex legal contract that provides financial protection against losses and damages to an individual’s house and assets in the home. It also provides liability coverage against accidents in the home or on the property.

Navigating the intricacies of insurance jargon can be daunting. However, understanding the core components, policy types, and exclusions is essential for ensuring that you are neither underinsured nor paying for unnecessary coverage. This article provides an in-depth exploration of the various facets of a standard homeowners insurance policy.

The Core Components of a Standard Policy

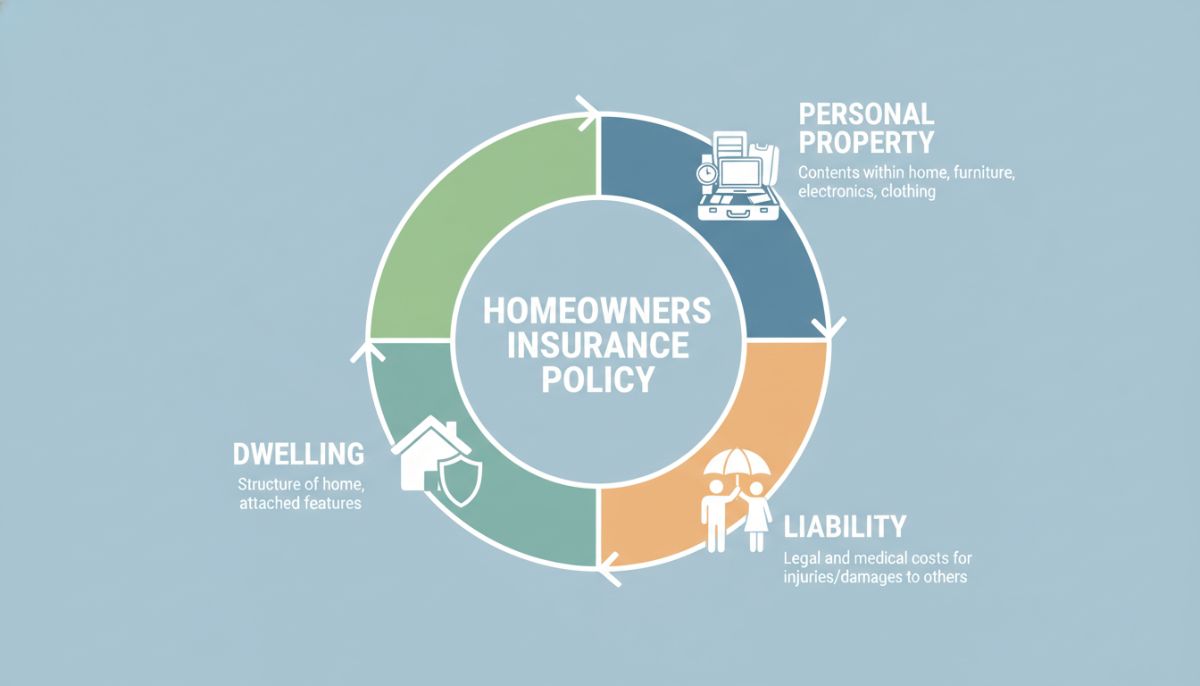

A standard homeowners insurance policy, often referred to as an HO-3 in the United States, typically comprises several distinct types of coverage. Each serves a specific purpose in the event of a claim.

1. Dwelling Coverage (Coverage A)

Dwelling coverage is the foundation of your policy. It pays to repair or rebuild the physical structure of your home if it is damaged by a covered peril, such as fire, windstorm, hail, or lightning. It is important to note that dwelling coverage should be based on the cost to rebuild the home—the replacement cost—rather than the market value, which includes the value of the land.

2. Other Structures Coverage (Coverage B)

This component covers structures on your property that are not physically attached to your house. Examples include detached garages, fences, tool sheds, and guest houses. Typically, the limit for ‘Other Structures’ is set at 10% of your dwelling coverage limit.

3. Personal Property Coverage (Coverage C)

Personal property coverage protects the contents of your home, including furniture, electronics, clothing, and appliances. This coverage often extends to items stolen or damaged while you are away from home, such as items in your car or a hotel room. Most policies provide personal property coverage at 50% to 70% of the dwelling limit.

4. Loss of Use Coverage (Coverage D)

If your home becomes uninhabitable due to a covered peril, Loss of Use (or Additional Living Expenses) coverage pays for the increase in living costs while your home is being repaired. This includes hotel stays, restaurant meals, and other expenses that exceed your normal cost of living.

Liability and Medical Payments

Beyond physical damage, homeowners insurance provides vital protection against legal and medical expenses arising from accidents on your property.

Personal Liability (Coverage E)

Liability coverage protects you if someone files a lawsuit against you for bodily injury or property damage caused by you, your family members, or even your pets. It covers both the cost of legal defense and any court awards up to the policy limit. Minimum limits usually start at $100,000, but many experts recommend carrying at least $300,000 to $500,000 in coverage.

Medical Payments to Others (Coverage F)

This coverage pays for minor medical expenses for guests injured on your property, regardless of who is at fault. It is intended to settle small claims quickly and prevent them from escalating into larger liability lawsuits.

Common Policy Types (HO Forms)

Insurance companies offer different levels of coverage through various policy forms. The most common include:

- HO-3 (Special Form): The most popular policy for single-family homes. It covers the dwelling for all perils except those specifically excluded (open perils) and personal property for specifically named perils.

- HO-5 (Comprehensive Form): Provides the broadest level of protection. It covers both the dwelling and personal property on an ‘open perils’ basis, meaning everything is covered unless specifically excluded.

- HO-4 (Renter’s Insurance): Designed for tenants, covering only personal property and liability, not the structure itself.

- HO-6 (Condo Insurance): Tailored for condominium owners, covering the ‘walls-in’ portion of the unit and personal property.

- Location: Proximity to fire stations, local crime rates, and susceptibility to natural disasters (like hurricanes) play a major role.

- Replacement Cost: The size, age, and construction materials of your home.

- Claims History: A history of frequent claims can lead to higher premiums.

- Credit Score: In many states, insurers use credit-based insurance scores to help determine risk.

- Safety Features: Smoke detectors, security systems, and impact-resistant roofing can often earn you discounts.

Understanding Deductibles and Limits

A deductible is the amount you agree to pay out of pocket before your insurance coverage kicks in. Choosing a higher deductible usually lowers your annual premium, but it increases your financial responsibility in the event of a claim.

Policy limits are the maximum amounts the insurer will pay for a covered loss. It is critical to review these limits annually to ensure they keep pace with inflation and rising construction costs. For high-value items like jewelry, fine art, or collectibles, standard personal property limits may be insufficient, requiring an ‘endorsement’ or ‘floater’ for additional protection.

Important Exclusions: What Is Not Covered?

It is a common misconception that homeowners insurance covers all types of damage. Most standard policies specifically exclude:

1. Floods: Coverage for rising water must be purchased separately through the National Flood Insurance Program (NFIP) or private insurers.

2. Earthquakes: This requires a separate policy or an endorsement.

3. Maintenance Issues: Damage caused by wear and tear, mold (in many cases), or pest infestations is generally considered the homeowner’s responsibility.

4. Sewer Backups: Unless you add a specific rider, damage from backed-up sewers or drains is often excluded.

Factors Influencing Premium Costs

Several factors determine the cost of your homeowners insurance premium:

Conclusion

A homeowners insurance policy is your primary defense against financial catastrophe. By understanding the nuances of Dwelling, Personal Property, and Liability coverages, you can make informed decisions that protect your family’s future. It is recommended to conduct an annual review of your policy with a qualified insurance agent to ensure that your coverage remains aligned with the current value of your home and assets. Investing the time to understand your policy today can save you from significant hardship tomorrow.